The A to Z of the Energy Transition: O is for Oil and Gas

As always (but particularly this week!) the views expressed are mine and not those of the Energy Institute.

I am proud to have spent much of my career working in the oil and gas sector. As a young engineer, standing on the Forties Unity platform with (at the time) nearly 700, 000 barrels of oil a day flowing under my feet I gained a palpable sense of the role the sector provided in meeting the UK's energy needs.

Globally, oil, plus coal and gas provides over 80% of energy globally (and before anyone jumps in, I'll be talking more about how we measure energy inputs and outputs in the next edition). Despite the perception that coal has long had its day, the world consumed more coal in 2024 than ever (and more of everything else). Fossil fuels have driven modern life as much of the world now enjoys, without which we wouldn't be able to travel round the world, heat our homes, light our schools and refrigerate our food and medicines.

But, it is interconvertible that in order to slow down global warming and limit the impact of climate change, we need to produce and consume a LOT less coal and oil. And maybe more, maybe less gas - at least in the short to medium term.

I'd like to talk about five aspects of the role of oil and gas in the energy transition:

1. Reducing operational emissions

2. The role of gas as a 'transition fuel'

3. Decarbonising embedded carbon from oil and gas

4. The role of the oil & gas workforce and supply chain

5. Whether there is ever a case for growing oil and gas production

Reducing operational emissions from oil and gas

Addressing the operational emissions from oil and gas production is sometimes portrayed as window-dressing by climate campaigners, as it largely focuses on scope 1 emissions and not the far larger embedded emissions from the carbon dioxide that is released when consumed, but this is to ignore an easy and short-term opportunity to make a material difference.

The Energy Institute Statistical Review of World Energy showed that emissions from production of oil and gas accounted for over 5 Gigatonnes of CO2 equivalent in 2024, that's around 13% of total emissions from energy. Furthermore, a lot of this is relatively low hanging fruit, through better design and operational performance. For example:

• Reducing flaring in oil and gas operations: flares are critical safety devices, to depressurise and burn off gas in the result of plant upsets, but worryingly remain routinely used in many parts of the world - in some instance because gas is an unwanted bi-product of oil production. This needs to be a legacy of history and The World Bank has set a target to eliminate routine flaring by 2030 (Zero Routine Flaring by 2030). Capterio, led by Energy Institute Fellow Mark Jonathan Davis, FEI, FGS is at the forefront of tackling this issue through its FlareIntel platform, Capterio provides real-time satellite-based analytics that track every flare globally, helping operators identify and prioritise opportunities for flare capture.

• Methane emissions: were covered in great detail by Yvette Manolas FEI in M is for Methane Emissions. The far more potent warming effects of methane (versus CO2) make this a massive priority. Programmes such as the United Nations' OGMP 2.0 (The Oil & Gas Methane Partnership 2.0) are critical in accelerating action. The Energy Institute played a significant role supporting Methane Guiding Principles

• Electrification of production facilities is another important approach, helping to avoid the use of diesel and fuel gas, particularly in offshore facilities. Norway is leading the way on this, electrifying much of its offshore infrastructure. Something the UK has yet to follow, although Equinor's Rosebank (if approved) will be powered from onshore electricity.

Beyond these areas, robust preventative maintenance and strong asset integrity (areas which the Energy Institute Technical & Innovation programme is heavily involved with) helps drive safer, more efficient and lower carbon operations.

The role of gas as a 'transition fuel'

It is widely understood that natural gas produces roughly half the CO2 emissions of coal and yet globally coal consumptions remains significantly higher than gas (165 EJ vs 149 EJ). And in power generation, coal still accounts for over a third of power generation (vs under a quarter for gas). According to the International Energy Agency (IEA) coal-to-gas switching avoided around 500 million tonnes of CO₂ emissions from 2010 - 2019 —equivalent to removing 200 million internal combustion engine vehicles from the road. In the UK, the 'dash to gas' in the 1980s and 1990s saw significant displacement of coal from gas, helping the UK to become the first major economy to halve its emissions by 2022. The US followed on the back of the shale revolution, which brought abundant and cheap gas. Between 2010 and 2024, US coal generation fell by nearly two-thirds and gas nearly doubled.

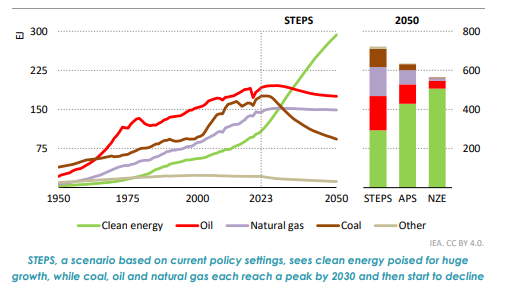

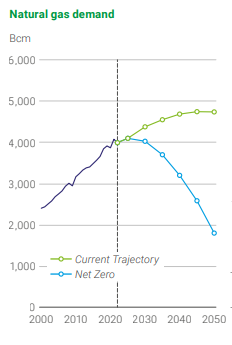

The key question on gas, is where and for how long does it accelerate the transition and at what point does it start slowing the transition. The outlook for gas demand has a far wider range of outcomes than coal or oil. Both bp and the International Energy Agency (IEA) show a wide variation in outcomes for gas out to 2050 (and of course there are other forecasts available). There's not space here to get into which scenario is most likely to prevail, but it is worth looking at the historic data to get some clues. Coming back to the UK and US, gas generation peaked in the UK way back in 2008. Since then renewables have displaced gas. Contrast this to the US, where despite the massive growth in renewables, gas generation reached an all-time high in 2024.

It's also important to remember that gas provides another critical role in generation, helping balance increasing variability from wind and solar. Whilst technologies such as battery storage and demand response play increasing roles, gas will continue to play the leading role in balancing the grid for many years to come.

Source: IEW World Energy Outlook (2024)

Source: BP Energy Outlook (2024)

Decarbonising embedded carbon from oil and gas

The first section covered the scope 1 emissions from production of oil and gas, but what about the embedded emissions from consumption of oil and gas?

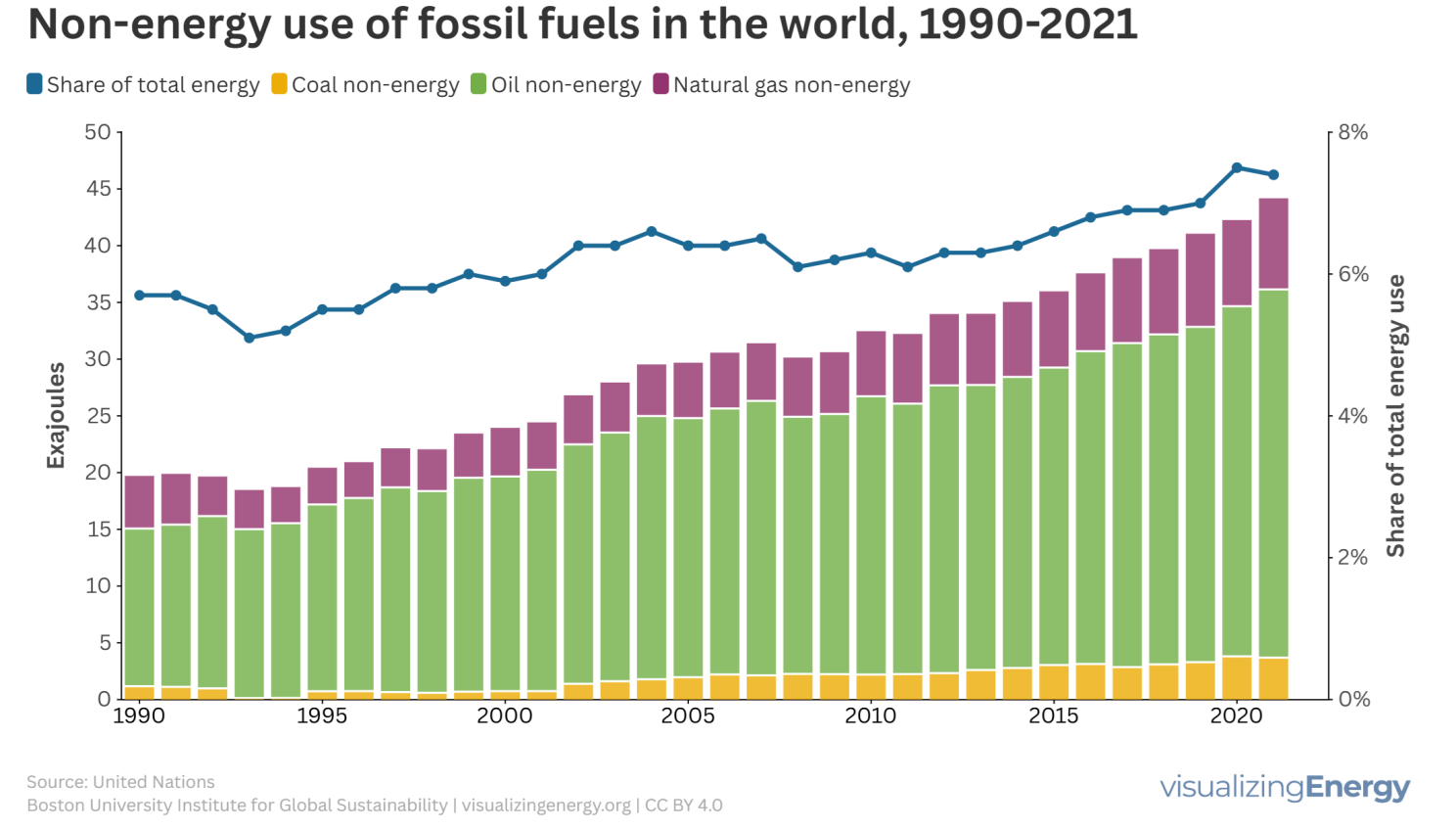

First, there is a very important point that not all oil, gas (and coal) is combusted. Around 8% of fossil fuels (largely oil-based) is used for non-combusted purposes, such as petrochemicals, fertilisers and bitumen etc. This figure is steadily increasing in both relative and absolute terms.

Non-energy use of fossil fuels - source Visualizing Energy, United Nations

However, the remaining 90%+ of fossil fuels are combusted and unless those emissions are captured, the go directly to the atmosphere. I covered this topic under C is for Carbon Capture.

It is exciting to see recent progress on CCUS projects, particularly here in the UK. CCUS has an important role to play, particularly around industrial clusters. However, we need to be realistic that at best it will capture a very small percentage of the CO2 emissions from oil and gas. Global capacity stood at under 60 million tonnes in 2024. Even assuming 100% operating capacity, this equates to capturing just over 0.1% of global emissions from energy.

The role of the oil & gas workforce and supply chain

Over 65 million people work in energy globally, with more than half already in clean energy. By 2030, 14 million new clean energy roles are expected to emerge, many of which will require post-secondary training. But it's really important there are pathways for those who continue to safely produce the oil and gas the world needs now.

There is huge transferability of skills and know how. The challenge is how people understand the opportunities, get the training and then land the right jobs. One of the real challenges in the UK is that oil and gas jobs are declining faster than new roles are emerging. Having visited Aberdeen a few weeks ago, there was a palpable sense of frustration and anxiety over the future.

Similarly, cities like Aberdeen have phenomenal engineering and supply chains capable of playing a major role in transition technologies, such as offshore wind and CCUS, but without clear pipelines of projects the danger is that companies decide to move elsewhere and once it's gone, it's probably gone forever.

Read more on this under J is for Just Transition.

Whether there is ever a case for growing oil and gas production

Finally, there has been a LOT of debate in the UK about the future of North Sea (and West of Shetland) oil and gas production. On one hand, some argue that the UK should lead by example and not permit new developments, such as the Rosebank project, to proceed.

On the other hand, others argue that as a net importer of oil and gas we should maximise the value to the economy and of course (to the previous point) maintain as many jobs for as long as we can.

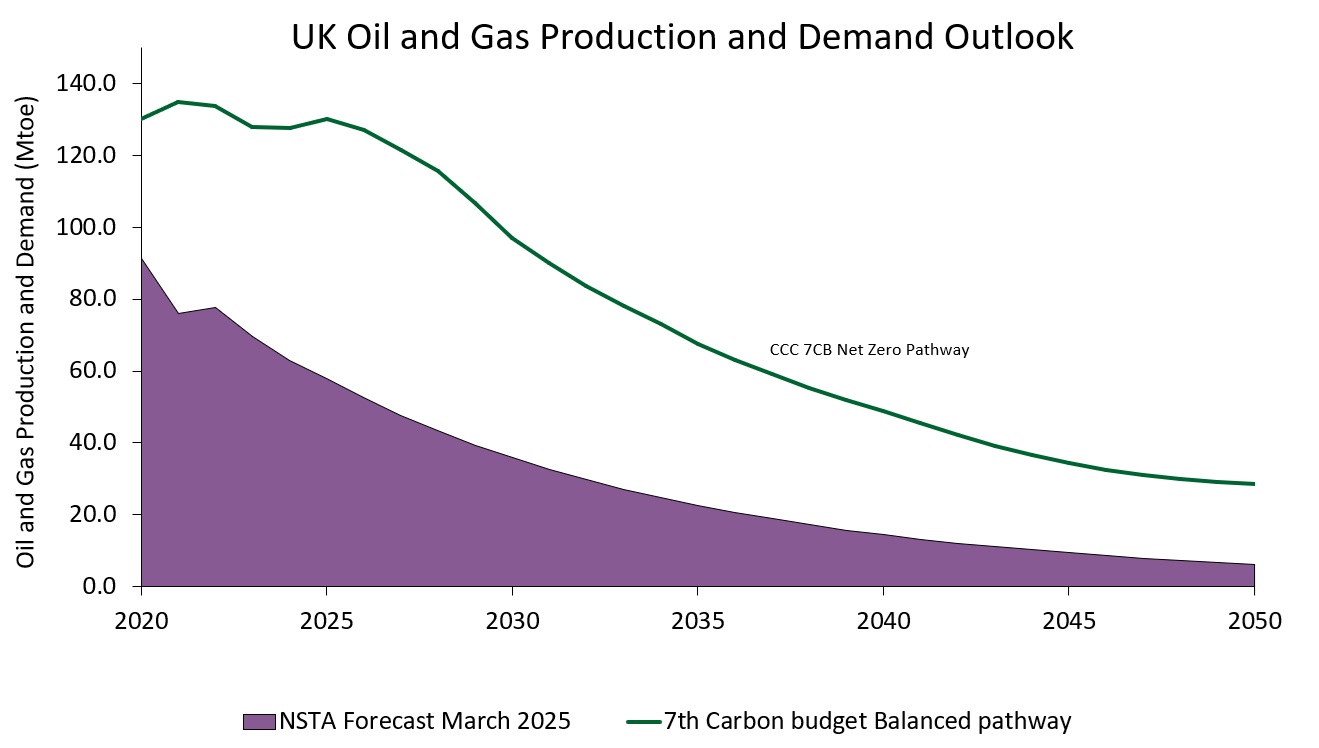

The UK only produces about half of the oil and gas it consumes. By 2050, even under the Climate Change Committee's 7th Carbon Budget (published earlier this year), the UK would be consuming around 40 Million tonnes of oil equivalent, around five times higher than the North Sea Transition Authority's forecast UK production for the same year.

The clear argument for supporting domestic production is that the gap in production is imported, often with higher emissions (for example from LNG versus pipeline gas).

My personal view on this topic is that the UK should continue to develop new projects, where they make commercial sense and so long as the highest standards are applied to operational emissions (i.e., zero routine flaring, offshore electrification etc.). For every barrel of oil and cubic metre of gas, there is a merit order on both cost and carbon. If the UK can compete on both, then I believe it should be allowed to - both for economic but also consistent with tackling climate change (as somewhere else a less economic, higher carbon barrel remains undeveloped). I wrote more on this topic in a piece last year: What if we imagined Planet Earth as one country?

I know not everyone agrees with this, but if we are serious about a just transition for people who live in cities like Aberdeen we need to do as much as we can to secure value for the economy and the workforce. Every year the North Sea is extended, it gives more hope of maintaining Aberdeen as not only the Energy Capital of Europe, but also becoming the Energy Transition Capital of Europe.

If you are interested in learning more about both sides of this debate please follow these links:

• Offshore Energies UK report on future of North Sea - https://oeuk.org.uk/policy-versus-geology-new-report-reveals-165bn-choice-facing-north-sea-future/

• A recent Cleaning Up Podcast featuring Tessa Khan - North Sea Oil & Gas Is Dying, What Comes Next? - Ep218: Tessa Khan

Further reading

As always, some further reading from the Energy Institute's New Energy World magazine, via Senior Editor Will Dalrymple.

Reducing operational emissions from oil and gas

Coal industry emits more methane than gas operations

What is needed to improve methane abatement in upstream oil and gas?

Methane: Time for our industry to accelerate action

Biggest methane-emitting oil and gas fields could reduce emissions significantly

Reducing flaring: six oil companies around the world show how it’s done

The role of gas as a ‘transition fuel’

Middle East to overtake Asia in gas output in 2025, predicts market report

Why Iraq still struggles to attract foreign investors in its energy and transition projects

New Indonesian President signs off $7bn gas project while reaffirming 2050 net zero target

Decarbonising embedded carbon from oil and gas

Decarbonisation challenges in the upstream sector

Decarbonising oil and gas operations

The role of the oil & gas workforce and supply chain

Retaking control: Africa boosts indigenous participation in oil and gas ventures

On the front lines of the skills shortage

Whether there is ever a case for growing oil and gas production

Emerging trends in the global oil and gas sector

Premium energy basins provide oil and gas as well as upstream decarbonisation opportunities