The A to Z of the Energy Transition: U is for Unabatable (or hard to abate)

Sorry, a bit of a clickbait title this time. 'U' was a difficult one, so please excuse the artistic licence in referring to hard (or expensive) to abate sectors as 'The Unabatables'. But just like prohibition-era Chicago, dealing with some of the hardest to decarbonise sectors is going to take grit and determination.

I've written a lot about the role of electrification in other letters (A is for Air source heat pump, Q is Queues for the Grid, R is for Renewable Energy, S is for Storage, T is for Transmission (& distribution), V is for Vehicles (electric ones!)) but what about all the parts of the economy that aren't so easy (or even impossible) to electrify? These are often described as 'hard to abate' sectors. Some are genuinely hard, in so much that there is not yet a technical solution that can be scaled to the extend required (think aviation - even if we everyone was willing to pay for sustainable aviation fuel, there simply isn't sufficient feedstock), whereas other sectors are technically feasible but just very expensive.

I had to start over on this piece, as I started getting into a lot of technical details on the merits and drawbacks of various solutions for different subsectors. The intention of this series was never to get highly technical and many others have written far more detailed pieces. So rather than trying to 'solve' each of these sectors I'll talk more about the relative emissions from each and a few of the technologies being developed to decarbonise them. I'll then go into a more conceptual discussion on how to think about the merit orders of 'problems' and 'solutions'.

What are the hard (or expensive) sectors to decarbonise ?

Aviation

Aviation accounts for around 2.5% of energy-related CO₂ emission.. The sector currently relies almost entirely on liquid fossil fuels - around 8 million barrels per day of jet fuel / kerosene (according to the Energy Institute Statistical Review of World Energy). Whilst aviation is a relatively small part of global emissions, it is the expected growth rate that is driving concern. International Air Transport Association (IATA) expect annual growth rates of 3.9% to 2034, with sustained growth thereafter. At that rate demand will double in less than 20 years. One of the most stark facts I've heard is that around 80-85% of the global population have never flown! I'm fairly confident that most of them would like to join the 15-20% of us who have.

So how we do decarbonise aviation? Electricity, hydrogen and SAF are all in the mix. Exciting advances are happening in the role of electrification of light aircraft, such as Robo taxis, and lightweight passenger planes. Gradually, these aircraft may get bigger and have longer ranges but it's very hard to see how they could ever manage intercontinental distances (absent some currently unforeseeable breakthrough in battery technology).

At the regional level, there are players looking at the potential roles of electric-hybrid planes and of hydrogen (or hydrogen derivatives. Heart Aerospace is developing a hybrid-electric 30-seat aircraft with 200 km of electric and 400 km of hybrid range. Heart Aerospace to Conduct First Fully Electric Experimental Flight in Plattsburgh, NY, Heart Aerospace

Developments are also taking place on the role of hydrogen for regional aircraft. Companies, including ZeroAvia are developing hydrogen-electric power trains that could potentially be retrofitted to aircraft such as the Dash 8. Producing, storing and handling liquid hydrogen is not going to be without its challenges, so it's a sector to watch closely. There are also developments underway in e-fuels, which combine hydrogen or biogas with a source of carbon dioxide to create chemically equivalent liquid fuels that could be dropped in to existing aircrafts. OXCCU TECH LTD is developing technology which combines biomethane and biogenic CO₂ into jet fuel. The biggest challenge to e-fuels is their cost, currently multiples more than their fossil equivalent.

And for the long-haul intercontinental travel, sustainable aviation fuel (SAF) remains the main focus of the sector. SAF is already blended into fossil aviation fuel at low percentages. The ReFuelEU Aviation Regulation has set a mandate starting with 2% in 2025, which increases to 70% in 2050. Two years ago a successful trial was completed with 100% SAF (The future of flight takes off as Virgin airliner crosses Atlantic solely powered by sustainable aviation fuel).

And as an important aside, the Energy Institute's Aviation Committee is doing a HUGE amount of work on handling, filtration and testing of SAF (and conventional fuels) - you can find out more here: Technical programme, Energy Institute

Shipping

Similar in scale to aviation, shipping is estimated to account for around 3% of global energy-related emissions. The maritime sector primarily uses heavy fuel oil, which is difficult to replace over longer distances due to energy density and storage constraints. Battery electric is beginning to play a role for shorter trips, particular point to point services such as ferries.

Ammonia and methanol are being explored as alternative fuels, but infrastructure and safety concerns remain. I enjoyed a tour of Fortescue's Green Pioneer ammonia-powered ship earlier this year Post / Feed / LinkedIn, which was very helpful in terms of understanding the level of safety systems to operate (ammonia is very toxic stuff). A.P. Moller - Maersk is pursuing a methanol as a solution (Maersk orders six methanol powered vessels). Both options have significant challenges to overcome if they are to be mainstream shipping fuels. I have to admit, I don't yet have a clear view on which is most likely to succeed.

Very topically, just last week the decarbonisation of shipping faced a significant setback with the delay on an International Maritime Organization vote to adopt the Net Zero Framework. IMO Postpones Adoption of Net Zero Framework, Delaying Global Action to Decarbonize Shipping

Shipping is growing more slowly than aviation (with around 0.5% growth expected this year, clearly not helped by trade wars). But there is also one very big difference compared with aviation: It is estimated that nearly 40% of global shipping cargoes are coal, oil, LNG and products. As we decarbonise other parts of the economy, this will begin to decline (according to the Energy Institute Statistical Review of World Energy, Chinese imports of crude oil fell in 2024). This means through time, a decent chunk of shipping emissions will largely be eliminated.

Steel

Steel is responsible for around 8% of global CO₂ emissions, it is highly carbon intensive due to the use of coking coal in blast furnaces - so emissions come from both the energy input and also the required chemical reaction to produce it.

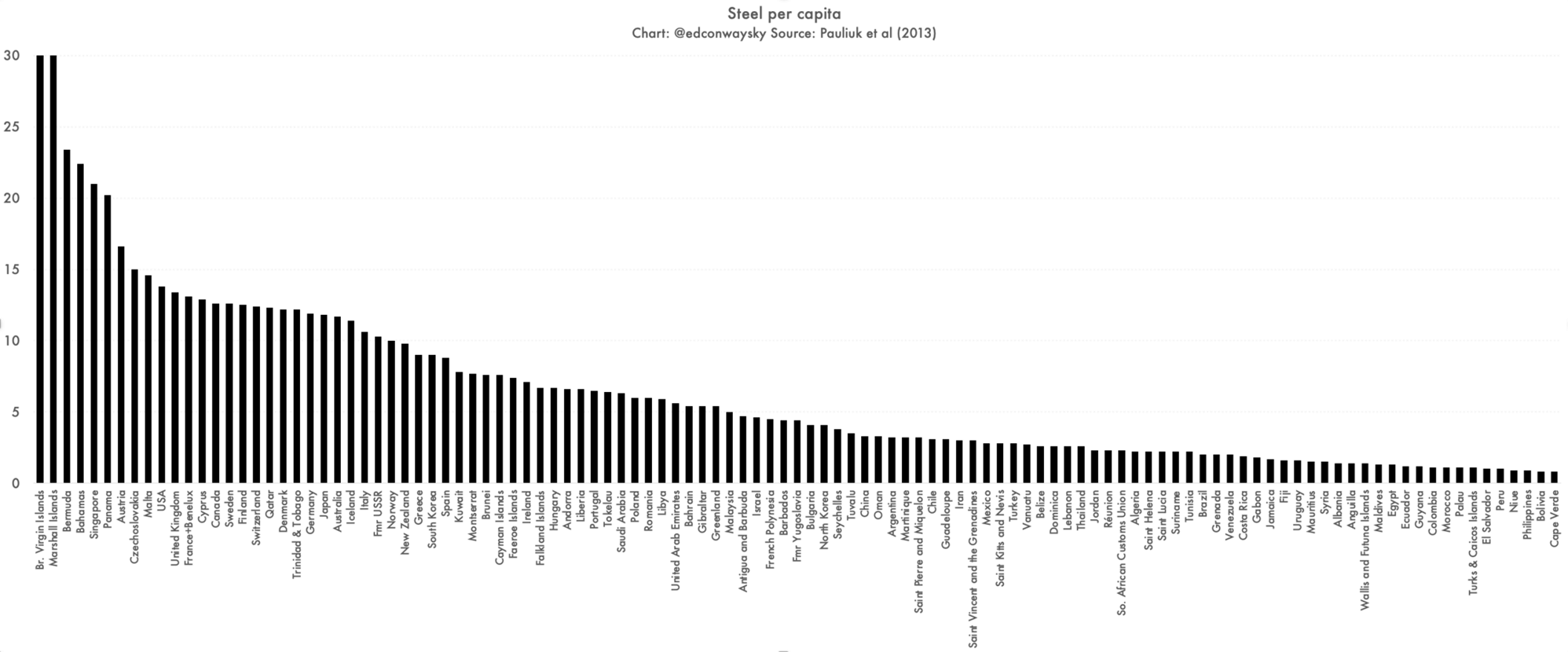

One of the starkest set of data on steel comes in the disparity between embedded steel across different economies. According to the brilliant Ed Conway (if you haven't read his book Material World, I'd highly recommend it), long-industrialised countries, like the UK and US, have between 10-15 tonnes of embedded steel per person. That's a lot! But then think about your car(s), the steel bars in your home, railways, schools, hospitals, bridges and it's not difficult to see how it adds up. Contrast that to middle income economies like China (3- 7 tonnes) and developing economies at less than a tonne (Mali and Niger are around 0.1 tonne). If every person on the planet wants to have as much 'stuff' as we do in the UK and US, that's a LOT of steel and a LOT of emissions to look forward to. The Best Datapoint of All,

Embedded steel per capita - Source: Ed Conway / Pauliuk et al (2013)

In terms of solutions, electric arc furnaces and green hydrogen-based direct reduction offer lower-emission alternatives, to produce 'green steel', these technologies are not yet widely deployed at scale and absent a carbon tax cost more than conventional production methods.

Cement

Cement produces a similar quantum of emissions to steel, at about 7% of the energy-related emissions. Its manufacture emits CO₂ both from the combustion of fossil fuels and the calcination of limestone (a chemical process intrinsic to cement production) to form 'clinker'.

Decarbonising cement is a complex and expensive challenge. One route is clinker substitution, where materials like fly ash, slag, or calcined clay replace a portion of clinker. Electrification of kilns and the use of alternative fuels—such as biomass or hydrogen—can also reduce fossil fuel dependence. CCUS (carbon capture use and storage) can also play an important role in capturing CO₂ from both clinker production and the production of heat.

I don't have a similar chart to the one above for cement, but wherever steel goes cement follows - be that on roads, buildings or railways lines - so the same disparities between developed and developing countries follow the same patterns.

Fertiliser and ammonia

Fertiliser production, particularly nitrogen-based fertilisers, involves significant emissions from ammonia synthesis produced from methane via the Haber-Bosch process, representing around 1-2% of energy-related emissions. Low-carbon ammonia can be produced using either blue hydrogen (from CCUS and gas) or green hydrogen.

Other hard to abate sectors

The above are some of the major hard-to-abate sectors, but clearly there are others including aluminium, glass, paper, brewing, all the way through to SMEs. What is common to most of these sectors, in contrast to steel, cement, shipping and aviation, is that they primary energy input is to create heat - which for the most part can be electrified, as both high-temperature heat pump and other forms of electrical heating technologies improve. The big challenge for these sectors is the cost of electricity, particularly in markets like the UK and Europe. The so called 'spark gap' the ratio between the cost of a kWh of gas and a kWh electricity is a major barrier to industries moving away from gas (a story which is playing out everyday in the UK media at the moment). If we solve the cost of electricity, we largely solve the problem of decarbonising these sectors.

The importance of merit orders

So I've given a brief summary of the key hard to abate sectors and a few of the technologies that are being developed to decarbonise them, but the big point I want to get across in this article is the importance of merit orders.

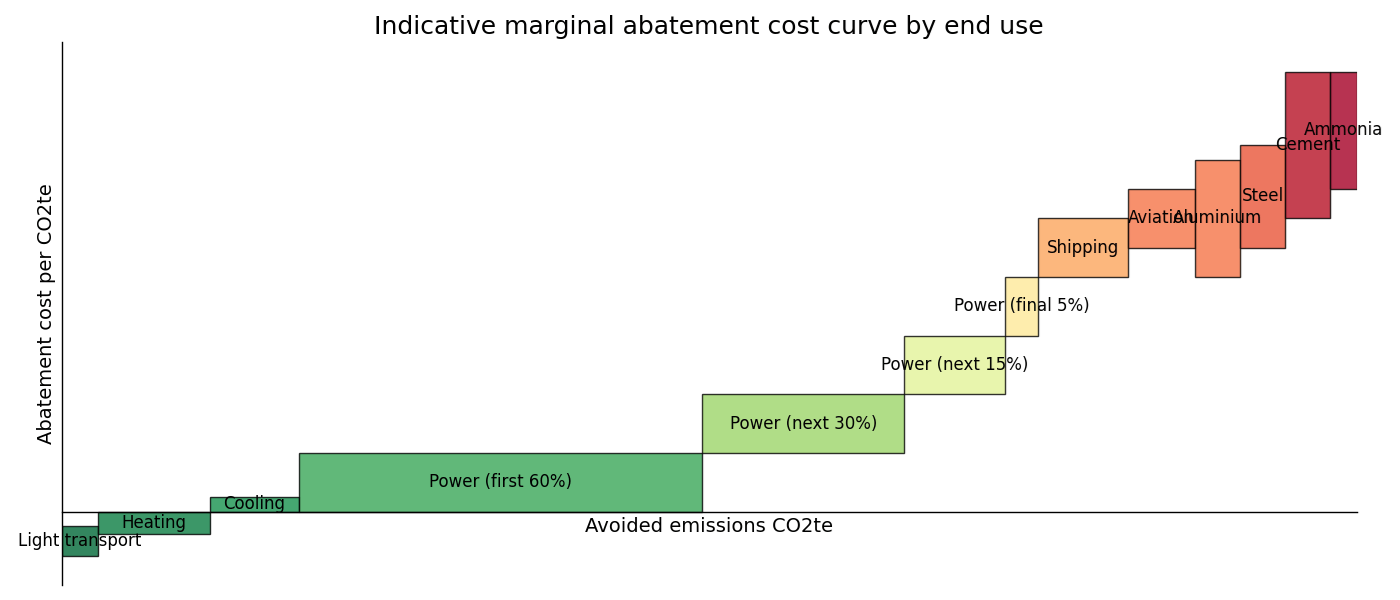

You may have seen a MACC (Marginal Abatement Cost Curves) chart. These show the relative cost per tonne of CO₂ equivalent and the relative size of each sector. There are lot you can pull of various websites, but I asked Microsoft Copilot to make a simple indicative one (based on real data). There are some sectors, such as light transport where the marginal abatement cost is negative - in other words, reducing CO₂ reduces costs (as I explored in V is for Vehicles (electric ones!), the lifecycle costs of an EV are typically lower than an ICE). Moving across the chart, the abatement costs become higher - through power, shipping, aviation, to steel, cement and ammonia. The merit orders vary regionally, so won't always follow this exact pattern but the overall picture remains broadly the same and of course there are interdependencies - the abatement cost for EVs will vary according to how clean or dirty the grid is.

Indicative marginal abatement cost curve (MACC) - created by Microsoft Copilot

Having discussed the merit order by end use 'problems', it's also important to think about the merit order for each 'solution'. A well-known example of this is Michael Liebreich's (who I happened to bump into on a plane just a few days ago!) Hydrogen Ladder Version 5.0 which shows the merit order use for hydrogen in different end uses. This really matters in some areas, for whilst green hydrogen could be used for high-temperature industrial heating, it would be far better used going into fertiliser or green steel. Similarly, whilst biofuels may be a really effective means of decarbonising cars in Brazil (where over 90% of new cars run on bioethanol), it may be a relatively poor use of those biofuels which would be better used in aviation, which has fewer choices. Practically, of course, it would be very challenging to tell all those Brazilian drivers they need to sell their biofueled ICEs and switch to EVs, so rich people can fly guilt free.

It's also really important to think about the merit order of the inputs to those solutions. So whilst making green steel may be a good use for green hydrogen, making green hydrogen might not be the best use of electrons. On a $ per unit of abated CO₂ those green electrons would be far better used decarbonising the grid and even better if they went into an EV or heat pump.

These merit orders throw up all manner of questions:

Does it make sense to focus on the right hand side of the above chart, until we've fully solved the left hand side? A dollar spent on decarbonising power will have far more benefit than the same dollar in aviation or shipping. Of course this doesn't mean we shouldn't undertake R&D for the technologies we'll need in the future, but we do need to be mindful of the trade offs. Arguably, could we ignore shipping for another 20 years, if that meant more focus on what has the biggest impact today ?

Conversely, is it right that aviation and shipping effectively get free rides at the moment, when so much effort is going into decarbonising grids. In the UK we're aiming for a 95% decarbonised grid by 2030, when aviation will at best be in single figures by then. A UK's household carbon footprint could be negligible with an EV and heat pump but completely wiped out by a holiday to Spain.

I mentioned above the differences in embedded quantities of steel and concrete between developed and developing countries. How do we ensure developing countries, like Mali and Niger are not priced out of building infrastructure when the developed West got a free emissions ride for the last two plus centuries?

How do we balance regional dislocations between merit orders, such as the Brazilian biofuels example above? Does it make sense for Brazil to carry burning all those biofuels in cars, or should efforts be made to electrify its car fleet to Europeans can fly guilt free?

- How are the relative costs of decarbonisation of these sectors ultimately borne by the end user and what is the proportional impact on the total cost? Whilst SAF is currently up to 5x the cost of fossil generated aviation fuel, it still represents a relatively small proportion of the total cost. KLM Royal Dutch Airlines recently introduced a 100% SAF surcharge on flights from Amsterdam to London City SAF: alternative aviation fuel - KLM GB - this adds €20 on way, so on a €100 fare it's material but not a game changer for most people. Similarly the cost of green steel might add a few hundred dollars to a $50k car - something most consumers would be willing and able to absorb. For sectors and shipping the cost of decarbonisation is relatively much higher - the question is then how those costs are allocated equitably, so as not to disadvantage countries or out whole sectors out of business.

- The one solution that would make all of this a lot easier is a single global carbon tax. This would ensure dollars flowed to where they were most impactful. In the absence of such a global carbon tax, the question is how far regional mechanism, such as the EUTS (EU Trading Scheme) and CBAM (Cross Border Adjustment Mechanism) can reach.

Conclusions

Just as Al Capone's empire felt unbreakable in 1930s Chicago, tackling the hard to abate sectors will require courage, determination and a joined-up approach. It also needs deep consideration on the order in which battles are won and fought. Whilst the announcement last week to push back a vote on a Net Zero Framework in shipping is a big blow, there maybe other areas where progress can and is already happening faster.

We need more that a single, Eliot Ness-esque, hero to this story. It needs energy professionals, technologists, policy makers and many others to find the optimal solutions to these challenges

And just like Capone, where despite his many heinous crimes it was tax evasion charges that finally got him caught, maybe, just maybe, one day we'll collectively realise that a global price on carbon is the most effective way to decarbonise even the hardest to abate sectors.

Further reading:

As always, further reading from the Energy Institute's New Energy World Magazine courtesy of Will Dalrymple

News

Research in hard-to-abate sector offers new possibilities to tackle climate change

Comment

Mineralisation – a carbon removal technology available today

Europe’s hydrogen paradox – balancing necessity, sustainability and economic feasibility

Hydrogen: a changing landscape but a promising future

Feature

Can hard-to-abate industries be decarbonised?

How an Italian steelmaker tackles waste heat recovery

Solid, gas and liquid: how carbon capture in cement production is becoming a concrete idea

Why renewable methanol is a cornerstone of global decarbonisation

Accelerating industrial decarbonisation: The Climate Club’s journey from COP28 to today