The A to Z of the Energy Transition: X is for (Power) to X

Disclaimer: This article was wholly written by AI! Microsoft Copilot was lead author and Claude reviewed and improved the flow. I challenged some of the language which was adjusted. I don't agree with everything 100% but I thought it would be interesting to explore how well AI could do this. I also asked Copilot to emulate my tone of voice, from previous articles. Please let me know what you think (unless you think it's done a better job than me in previous letters!)

If you're interested in the broader context of decarbonising hard-to-abate sectors, I encourage you to read my the recently published: U is for the Unabatables (or hard to abate)

The Challenge: When Plugging In Isn't Enough

Here's the problem: renewable electricity is booming, but roughly 30% of global energy demand comes from sectors that can't simply plug into the grid. Try running a container ship across the Pacific on batteries, or heating a cement kiln to 1,450°C with a heat pump. These hard-to-abate sectors—aviation, shipping, steel, cement, and chemicals—account for nearly a third of global CO₂ emissions, yet lack viable electrification pathways.

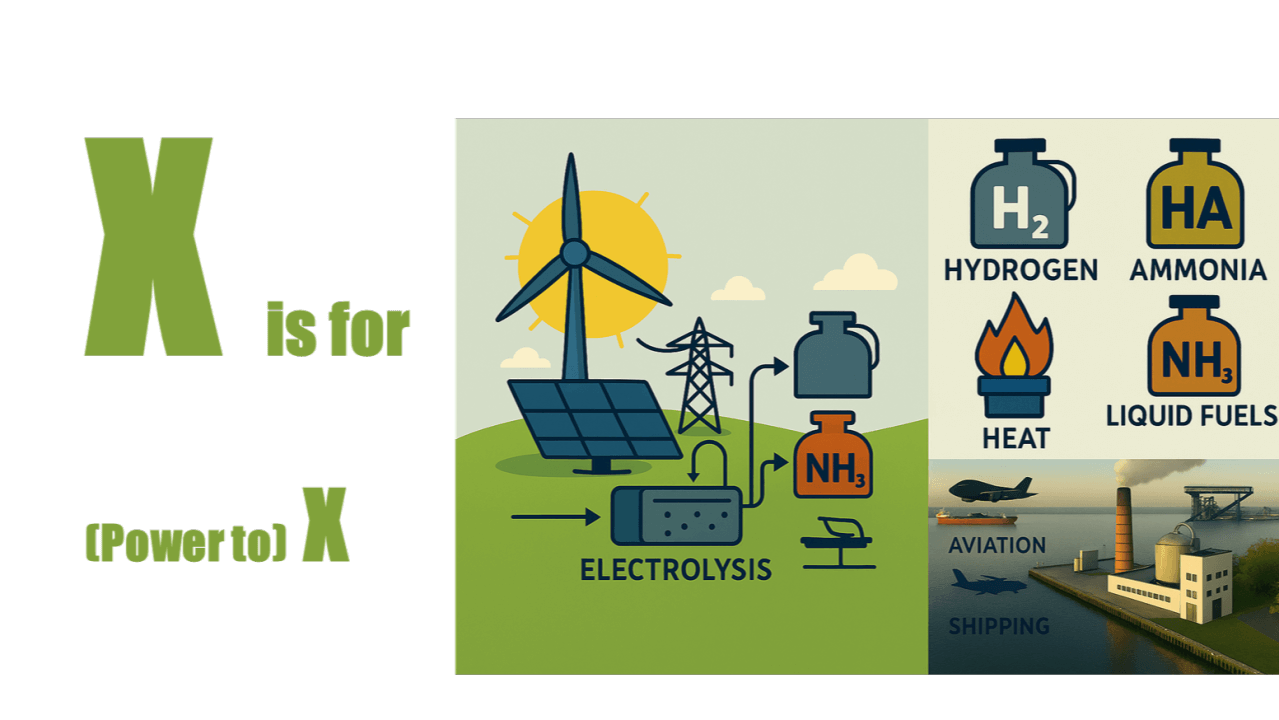

Power to X (PtX) is a potential answer, but not the answer to everything. It's a suite of technologies that converts renewable electricity into hydrogen, synthetic fuels, chemicals, and heat—creating molecules where electrons alone won't suffice.

How Power to X Works

The process typically begins with electrolysis: renewable electricity splits water into hydrogen and oxygen. This "green hydrogen" becomes the building block for multiple pathways:

- Power-to-Hydrogen: Direct use in fuel cells, steelmaking (replacing coking coal), or as an industrial feedstock

- Power-to-Gas: Hydrogen combined with captured CO₂ to create synthetic methane for existing gas infrastructure

- Power-to-Liquids: Hydrogen and CO₂ synthesised into e-kerosene for aviation or e-diesel for shipping

- Power-to-Ammonia: Hydrogen combined with nitrogen for fertiliser production or as a carbon-free shipping fuel

- Power-to-Heat: Direct electric heating for industrial processes or district heating systems

Real projects are already emerging: Maersk has ordered twelve methanol-capable container ships anticipating e-fuel availability, while Airbus is testing aircraft on 100% sustainable aviation fuel blends. Germany's GET H2 Nukleus project aims to create a 130km hydrogen pipeline network connecting industrial users by 2025.

The Efficiency Reality: Why PtX Isn't For Everything

Here's the uncomfortable truth: every conversion step loses energy. Electrolysis captures 60-70% of input electricity as hydrogen. Synthesising that hydrogen into fuels retains another 60-80%. If you then burn that fuel to generate electricity, you recover just 35-50% of what you started with. Full round-trip efficiency? Around 30-40%.

Compare this to a battery electric vehicle at 80-90% well-to-wheel efficiency, and the case for PtX seems weak. But this comparison partly misses the point. For sectors producing steel, flying planes, or manufacturing ammonia, we're not converting back to electricity—we're replacing fossil molecules with green ones. The alternative isn't a battery; it's continued fossil fuel combustion. In this context, PtX becomes essential rather than inefficient.

The challenge is cost. Green hydrogen currently costs $4-7/kg versus $1-2/kg for grey hydrogen from natural gas. E-fuels run 3-5 times more expensive than fossil equivalents. PtX only becomes competitive with abundant ultra-cheap renewables (below $20/MWh), high carbon prices (above $100/tonne), or regulatory mandates.

The Strategic Framework: PtX's Merit Order

Not all applications of PtX are created equal. A clear hierarchy emerges:

Tier 1 - Direct Electrification First: Heat pumps for buildings, electric vehicles for passenger transport, electric arc furnaces for recycled steel. If it can be electrified directly, it should be. The efficiency advantage is overwhelming.

Tier 2 - PtX for Hard-to-Abate Sectors: Long-haul aviation, deep-sea shipping, primary steelmaking, high-temperature industrial heat. These sectors have no credible alternatives and must use PtX despite the efficiency penalty.

Tier 3 - PtX for Long-Duration Storage: Seasonal energy storage where batteries are uneconomical. Hydrogen in salt caverns or synthetic methane can store summer sunshine for winter heating, supporting grid resilience.

Never - PtX Where Electrification Works: Heating homes with hydrogen boilers or running passenger cars on e-fuels wastes scarce renewable electrons. Germany learned this lesson when it abandoned hydrogen heating mandates in favour of heat pumps.

This merit order must guide deployment. Misallocating limited renewable capacity to low-value PtX applications delays decarbonisation of sectors with no alternatives.

The CO₂ Question: Where Does Carbon Come From?

PtX pathways requiring CO₂ face a critical challenge: sourcing sustainable carbon. Three options exist:

- Biogenic CO₂ from biomass or waste (limited availability, competing uses)

- Industrial point sources from cement or steel (only helps if those facilities continue operating)

- Direct air capture (energy-intensive and expensive, though improving)

This matters enormously for carbon accounting. E-fuels using fossil CO₂ from existing industrial processes only work if those processes are essential and can't be eliminated. Direct air capture offers true carbon neutrality but roughly doubles production costs. The source of CO₂ isn't a footnote—it's fundamental to whether PtX delivers genuine decarbonisation.

Geography Matters: The Renewable Advantage

PtX economics vary dramatically by location. Chile's Atacama Desert or Australia's Pilbara region can produce renewable electricity below $15/MWh—cheap enough to make green hydrogen competitive. Northern Europe, with offshore wind at $40-50/MWh, struggles with costs but has existing industrial infrastructure and demand.

This creates two models: produce PtX products where renewables are cheapest and ship them globally, or produce locally despite higher costs to leverage existing infrastructure. Both approaches are emerging, with the Middle East and North Africa positioning themselves as future e-fuel exporters.

Realistic Timeline and Outlook

PtX costs are falling but remain stubbornly high. Green hydrogen may reach $2-3/kg by 2030 in optimal locations—competitive with grey hydrogen under moderate carbon pricing. E-fuels need another decade and substantial carbon prices (above $150/tonne) to compete without subsidies.

Policy support drives deployment: the EU's renewable fuel mandates for aviation, contracts for difference schemes in Germany, and production tax credits in the US Inflation Reduction Act. Without these interventions, PtX remains uneconomical.

The technology is ready; the economics aren't—yet. Scale, learning curves, and policy will close the gap, but PtX is a 2030s and 2040s solution, not a 2020s saviour.

The Bottom Line

Power to X is neither silver bullet nor dead end. It's a necessary tool for decarbonising sectors where alternatives don't exist, but it's expensive and inefficient enough that we must deploy it strategically. The merit order matters: electrify everything possible first, then use PtX judiciously where nothing else works.

As renewable capacity expands and costs fall, PtX will play a targeted but vital role in achieving net zero. The question isn't whether we need it—we do. The question is where, when, and how much. Get that right, and PtX becomes the bridge between our renewable electron abundance and the molecules hard-to-abate sectors require.

Thanks Copilot and Claude!

Further reading:

As always, some further reading below (collated by a real human, Will Dalrymple MEI Senior Editor of the Energy Institute's New Energy World.

News

New EU platform to raise European green hydrogen production

Europe achieves e-fuels milestones as large-scale PEM and e-methanol plants begin production

For the nascent e-fuels industry, four steps forward, one step back

World’s largest green ammonia plant powered by off-grid renewables comes online in China

Oman integrates flagship project into national hydrogen strategy

Comment

Balancing supply and demand is key to kickstarting the green hydrogen sector

Hydrogen: a changing landscape but a promising future

Feature