The A to Z of the Energy Transition: L is for Lithium and other critical minerals

As the energy transition accelerates, there is an increasing focus on a relatively new class of natural resources: critical minerals. These include lithium, cobalt, nickel, copper, graphite, and rare earth elements—all materials essential to the technologies underpinning the energy transition.

From electric vehicles and battery storage to wind turbines and solar panels, these minerals play a critical role in decarbonisation. Yet, their rising demand, geopolitical concentration, and environmental implications pose challenges that must be addressed to ensure a just and sustainable energy transition.

Lithium, often dubbed “white gold,” is central to lithium-ion batteries, which power everything from smartphones to EVs and grid-scale storage systems. Cobalt and nickel enhance battery performance and longevity, while rare earth elements are vital for the permanent magnets used in wind turbines and EV motors. Copper, with its high conductivity, is critical for electrical infrastructure, including transmission lines, as well as generators on wind turbines.

As a side note, it's worth noting that many of these materials and others have long played a crucial roles in things like catalysts in fossil energy - for example, the valuable platinum in catalytic convertors on petrol / gasoline cars has led to a spate of thefts from cars in the UK.

Production and reserves

According to the International Energy Agency (IEA) Global Critical Minerals Outlook 2025, demand for these minerals is projected to soar. Under the IEA Net Zero Emissions by 2050 Scenario (NZE), lithium demand could increase more than sevenfold by 2040, while demand for copper and nickel could more than double. This surge is driven by the electrification of transport, expansion of renewable energy, and the digitalisation of energy systems.

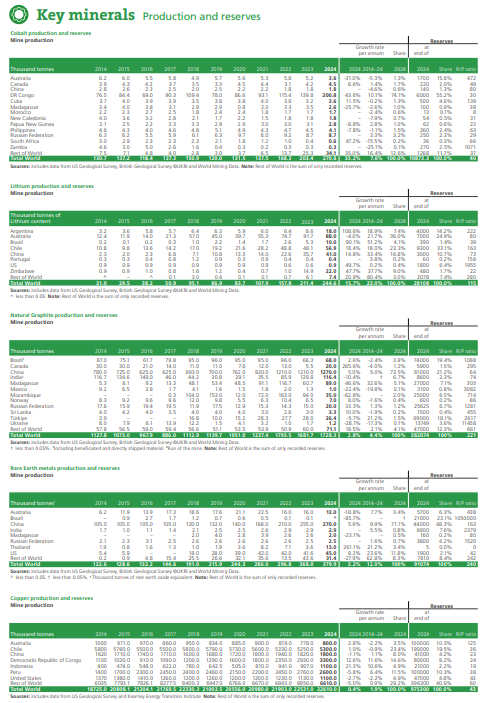

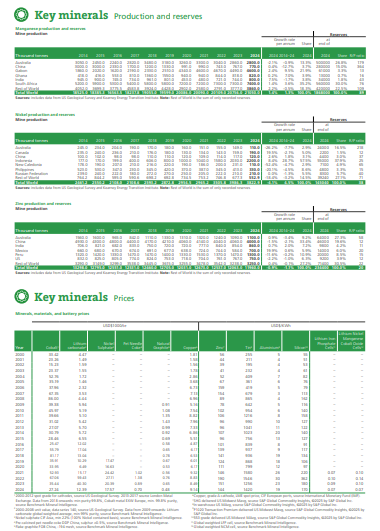

In the Energy Institute Statistical Review of World Energy (published just yesterday, on 26th June) we track the latest data on key production and reserves. I've copied over some of the key data tables below but the headlines are as follows:

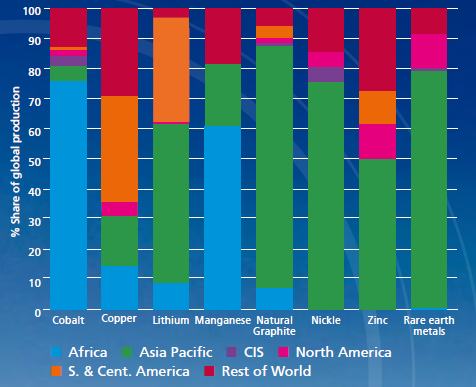

• Global rare earth metals mining increased by 3.2% in 2024 reaching 0.4 million tonnes. China maintained its dominance accounting for 71% of global production and 48% of worldwide reserves.

• Global production of lithium increased by 16%. Chile continued to be the second-largest lithium producer with a 23% share of global output. Its production grew by 18%, whilst Argentina saw a significant increase of 109%.

• On average, key mineral prices fell globally by 16% in 2024 with the biggest falls in lithium carbonate (-69%), natural graphite (-26%), and cobalt (-23%)

Concerns are increasingly being raised on the reserve to production ratios (R/P) of key minerals. Again, the Energy Institute Statistical Review of World Energy tracks data on reserve volumes. Reserve to production ratios vary dramatically across key minerals: 20 years for zinc, 43 years for copper and 221 years for graphite (you can see all the figures in the tables below).

However, these ratios should be handled with some caution (a large pinch of lithium, if you will). On the one hand, measuring an R/P ration, with a relatively static 'R' but exponentially growing 'P' can dramatically over state an expected reserve life. On the other hand, geologically we are unlikely to run out of physical reserves anytime soon - once resources are discovered, the challenge is proving that they are commercially viable for production in order to be classified as reserves. So this is less about what is in the ground and more about above ground challenges to extract resources economically.

A similar dynamic played out with coal, oil and gas - all of which were forecast to reach peak supply at some point around the turn of millennium. In reality, advances in technology (e.g., deep water, shale and LNG) and price have dramatically extended the reserve life of fossil fuels, and I have little doubt that a similar trend will follow for critical minerals to the point that it is very clear that it is peak demand, rather than peak supply which will determine how much is ultimately extracted.

Supply Chain Vulnerabilities and Geopolitical Risks

Despite their importance, the supply chains for critical minerals are generally highly concentrated. For instance, nearly a quarter of the world's copper comes from Chile, over a third of lithium is currently produced in Australia and the Democratic Republic of Congo dominates three-quarter of global cobalt production.

It's important to remember that it's not just where the minerals are found but where they are processed, which is potentially even more important. Whilst Australia is the largest source of lithium, China absolutely dominates processing of it. These concentrations are creating increasing geopolitical tensions, trade restrictions, and supply disruptions. Just a couple of months back, access to Ukraine's critical minerals was a key component of a 'deal' with the US administration.

The International Energy Agency (IEA) warned that the average market share of the top three refining countries rose to 86% in 2024, up from 82% in 2020. This trend runs counter to the principle of diversification, as a cornerstone of energy security. The risk is particularly acute for copper, where a projected 30% supply deficit by 2035 could slow the deployment of expanding transmission and distribution networks.

In 2024, the Asia Pacific and Africa regions produced 57% of the key metals and materials needed by the global energy system.

Source: Energy Institute Statistical Review of World Energy 2025

Environmental and Social Considerations

Mining and processing critical minerals come with significant environmental and social risks that need to be managed. These include land degradation, water use, carbon emissions, and impacts on local communities, including working conditions, child labour and health & safety issues. It is critical that supply chains work to ensure higher standards from mine to end use. And clearly, each of us as consumers has a role to play in asking questions on the sourcing of materials for our EVs and iPhones etc.

An Energy Institute 2021 webinar on decarbonising critical minerals mining highlighted the need for digital technologies and ecosystem collaboration to improve sustainability across the value chain.

There are also some confusing messages on recycling rates of lithium ion batteries. These are often misleading comparing the rate of recycling to the rate of production - clearly with battery lives often exceeding a decade, recycling rates won't catch up with production rates for many decades. The good news is that there are very strong commercial incentives to reuse or recycle batteries and if you want to learn more on this topic, do listen to the excellent edition of the Cleaning up podcast (link below) when Michael Liebreich interviews leading global expert Hans Eric Melin. So next time you hear somebody say that only X% of batteries are recycled, please do challenge them for the data!

Technological innovation is another factor in reducing dependency on single materials. Advances in battery chemistry, such as solid-state and sodium-ion batteries, could reduce reliance on scarce minerals like cobalt and lithium. Meanwhile, digital technologies are enabling more efficient exploration, mining, and processing, as well as better tracking of material flows.

This is a HUGE topic, which I've not done full justice to, so would love to see what YOU have to say in the comments. And please do share links to other interesting articles.

If you would like to learn more, I'd really recommend Ed Conway's excellent book, Material World, which provide a fascinating insight into the world of how some of these critical materials (including copper and lithium) are extracted, processed and brought to market. It's a brilliant read.

Appendix: Highlights from the Statistical Review of World Energy

Source: Energy Institute Statistical Review of World Energy

Source: Energy Institute Statistical Review of World Energy

Further reading (and listening):

News article about February 2025 IEA report on critical materials, including lithium

News article about report on lithium mining in Africa

Feature article about the lithium mining supply chain, with a focus on primary exporter Australia

Energy Institute Energy Insight: Energy storage - battery technologies

Ed Conway's brilliant book Material World https://www.amazon.co.uk/Material-World-Substantial-Story-Future/dp/0753559153

Further listening

Cleaning up Podcast: Julie Klinger 'Rare Earths, Real Insight'

Cleaning up Podcast: Material World, Ed Conway

Cleaning up Podcast: Battery Recycling Is Here - But Where Are The Batteries? - Hans Eric Melin

Online Resource details

Websites:

Link to LinkedIn post

Keywords: A-Z energy transition

Subjects: Lithium, Rare earth materials/Critical minerals