New Energy World™

New Energy World™ embraces the whole energy industry as it connects and converges to address the decarbonisation challenge. It covers progress being made across the industry, from the dynamics under way to reduce emissions in oil and gas, through improvements to the efficiency of energy conversion and use, to cutting-edge initiatives in renewable and low-carbon technologies.

Exploring China’s enormous green energy shift

5/6/2024

8 min read

Feature

Today, China has 18% of the world’s population, uses 26% of global primary energy, emits 33% of global energy-related CO2, and is by far the leading installer of renewables. The energy transition in China is critical to its future and to the success of the global energy transition, according to a new report from DNV, Energy Transition Outlook China,* of which an edited summary and extract is republished here.

China is establishing itself as a green energy leader with an unrivalled build-out of renewable energy and export of renewable technology. On the other hand, DNV forecasts fossil fuels will still account for 40% of its energy mix in 2050.

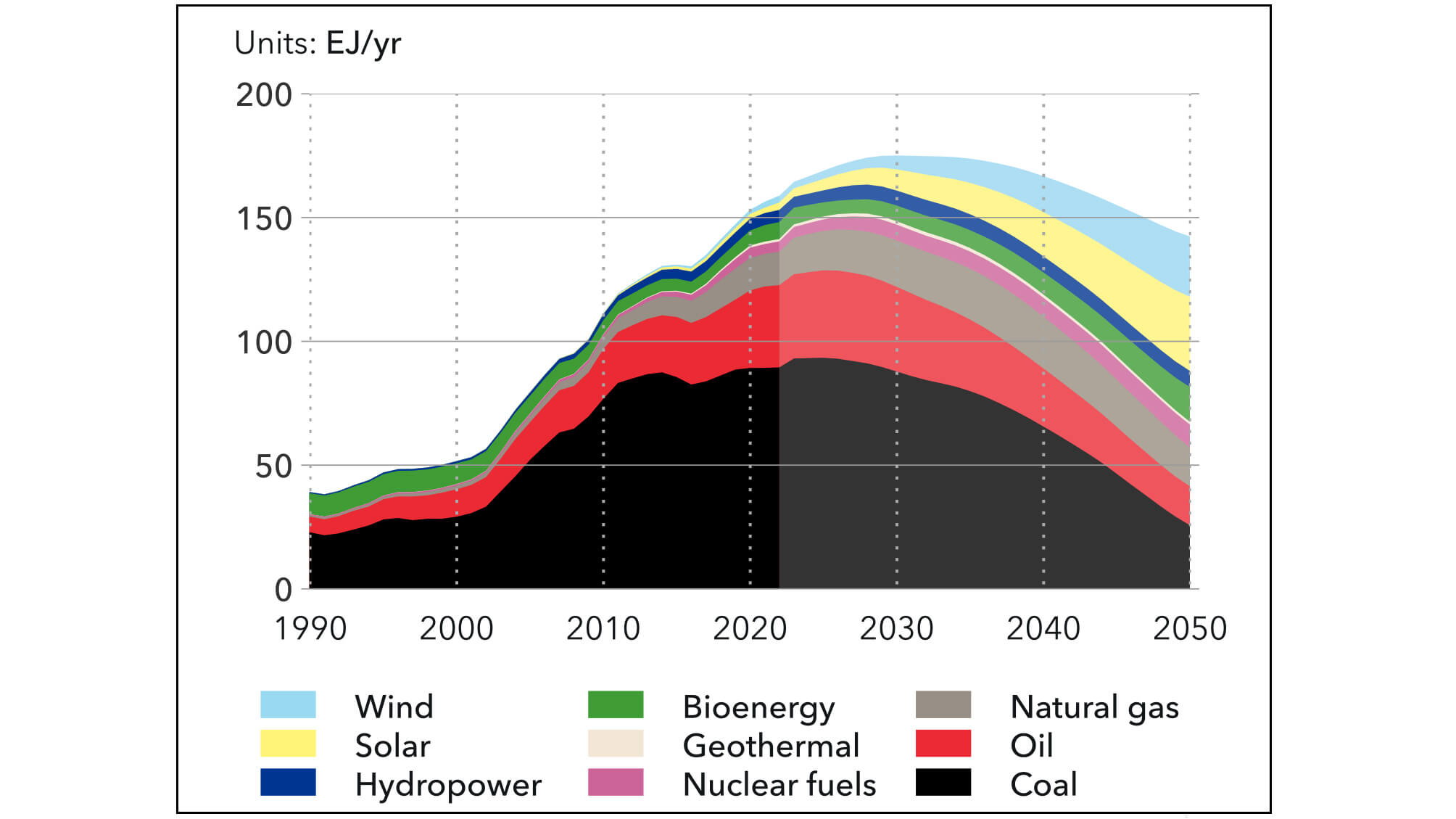

Energy independence is a key motivation for Chinese energy policy, but it will be only partly achieved. The power sector is decarbonising quickly by replacing coal with domestically sourced renewable energy, and domestically produced coal will largely be sufficient for the remaining coal demand segments by 2050 (see Fig 1).

However, oil and gas usage will continue to rely on imports. Although oil consumption halves by 2050 from its 2027 peak in our forecasts, its use in petrochemicals and heavy transport (aviation and shipping) will linger and 84% of oil use will be met through imports. Natural gas consumption will remain high, with 2050 consumption marginally below 2023 levels and 58% being imported.

Strong policy support is reflected by the rapid uptake of green technologies. China, already a leader in renewable energy investments, will more than quintuple renewable energy installations by 2050. In 2010, wind made up only 1% of China’s electricity generation. However, policy has turbocharged the sector, and today wind is China’s largest source of electricity after coal and hydropower, delivering 9.4% of the total electricity supply in 2023. By mid-century, it will comfortably be the world’s largest wind market.

Likewise, solar made up less than 1% of power generation in 2015 and in less than a decade this has risen to 5% today. Solar and wind will each contribute 38% of electricity production by 2050.

Fig 1: China’s primary energy supply by source, in EJ/y – coal consumption in China is predicted to peak in the next year or two and fall to a quarter of peak value by 2050

Source: DNV's Energy Transition Outlook China, 2024; historical data source IEA, 2023

Leveraging cost reductions and sustained global exports, China is poised to assist the rest of the world in meeting its renewable energy targets, exporting solar panels and most likely also wind turbines to most parts of the world.

‘Intense policy focus and technological innovation is transforming China into a green energy powerhouse,’ says Remi Eriksen, Group President and CEO of DNV. ‘There is much to admire about China’s energy transition. There are visible signs of a vast decarbonisation effort and clean technology development within renewable energy, storage and transmission technologies. However, there is potential for China to push further its transition to reduce its reliance on fossil fuels further and faster – and to bring China closer to net zero emissions by 2050.’

China’s energy use will peak by 2030 and reduce by 20% by 2050, driven by electrification and energy efficiency improvements. This decline is also enabled by demographic shifts, including a projected 100 million population decrease.

Of the 10 world regions in the DNV energy transition outlook forecast, China currently ranks as sixth in terms of electrification of demand, but it is projected to rise to second place, comprising 47% of final energy demand by 2050, surpassing Europe and North America and trailing behind only OECD Asia-Pacific.

From a position where, in 2023, China was responsible for a third of the world’s energy-related CO2 emissions, by 2050 that share will have reduced to a fifth. In absolute terms, China’s emissions will reduce by 70%, following a path close to meeting its target of carbon neutrality by 2060.

Given the weight of China’s contribution to global emissions, the timing and depth of China’s emissions reduction are of immense importance globally. The net-zero trajectory for China outlined in DNV’s 2023 Pathway to Net Zero report shows that China’s cumulative emissions could be 113 GtCO2 lower than expected, significantly aiding global efforts to reach net zero by 2050.

‘Intense policy focus and technological innovation is transforming China into a green energy powerhouse. There is much to admire about China’s energy transition. There are visible signs of a vast decarbonisation effort and clean technology development within renewable energy, storage, and transmission technologies.’ – Remi Eriksen, Group President and CEO of DNV

Coal

Coal consumption has nearly peaked in China. Between 2000 and 2010, there was a substantial surge in coal demand, rising at an annual growth rate of 10%, from 1,351mn tonnes to 3,526mn tonnes. More modest growth followed over the next decade, with demand reaching 4,100mn tonnes by 2022, followed by a 5% leap in 2023, according to International Energy Agency (IEA) figures. We forecast a minor uptick in total coal consumption over the next two years, before falling by a third by 2040 and ending at some 25% of peak coal use by 2050.

In 2023, China prioritised short-term energy security to avoid a recurrence of the power shortages that occurred in 2021 and 2022. This led to an increase in thermal coal imports, with shipments from Indonesia up 65.9% year-over-year to 89.9mn tonnes, as well as increases in shipments from Russia and Australia. We forecast a minor increase in total coal consumption over the next two years, before a decline to 3,005mn tonnes by 2040 and to 1,176mn tonnes by 2050.

Anticipating the decrease in coal-based power generation and the swift expansion of renewable energy sources, coal plants will experience reduced revenue due to lower utilisation. The National Development and Reform Commission (NDRC) has therefore developed mechanisms to compensate coal power plants for losses as they adjust to their new role as backup suppliers.

China’s rapid additions of new coal-fired power plants and its lack of a coal phase-out plan are responsible for it falling behind the Paris Agreement pace, despite the country’s record buildout of renewable energy. In 2021, China’s President Xi Jinping stated that the country would start ‘phasing down’ coal use, starting in 2026, as part of its effort to slash carbon emissions and reach carbon neutrality by 2060.

However, China has been adding coal capacity at a record pace: in 2022, 86.6 GW of new coal-fired power plant capacity was approved compared with 18.6 GW in the previous year, and in the first half of 2023 an average of two plants per week were approved, adding 52 GW of new coal-fired capacity.

In 2021, China announced it would stop financing and supporting technology for coal plants overseas. This is an important step that increases the costs of new coal-fired generation in other regions and helps the transition to cleaner technologies. According to Global Energy Monitor, overseas coal project financing by China in 2022 had fallen 78-fold since its peak at $39bn in 2017.

On the demand side, the power generation and manufacturing sectors are the major coal consumers in China. According to the outlook, coal consumption in both sectors will continue growing for the next two years, but afterwards coal’s share in electricity generation will reduce from 60% today to less than 25% by 2050, and is predicted to continue to drop to a low of 3% in the century. The electrification of China’s manufacturing is projected to decrease demand from 29 EJ in 2022 to 13.6 EJ by 2050, with iron and steel production expected to constitute the highest share of coal demand at 35% in 2050.

However, the economic appeal of transitioning to electric arc furnaces is hindered by the relatively new status of many basic oxygen furnace facilities in China. Towards the end of the outlook period, iron and steel (9 EJ/y) will overtake power generation (7 EJ/y) as the largest consumer of coal in China. Coal use in buildings, which is relatively small, will fall in the coming years to be largely replaced by natural gas. Coal demand in non-energy (feedstock) remains quite stable. In China, over the past two decades, coal gasification has played a pivotal role in producing methanol, ammonia and hydrogen (as feedstock). As of 2022, coal fuelled approximately 66% of the hydrogen (as feedstock).

If China’s coal use follows the path in our forecast, the resulting annual emissions from coal will fall from 8 GtCO2 in 2022 to 1.8 GtCO2 in 2050, making a crucial contribution to reducing global emissions. Yet, China’s coal-related emissions, comprising 11% of global energy-related emissions in 2050, stand as a significant barrier to achieving worldwide net zero emissions by mid-century. To achieve the 1.5°C target, the share of coal in China’s power mix must be significantly reduced to single digits by 2035, and a complete phase-out of coal should be considered by 2045, as outlined in DNV’s 2023 Energy Transition Outlook report.

*This article was based on DNV’s 124-page Energy Transition Outlook China report.

- Further reading: ‘Global visions: International Energy Week debates the key factors impacting the energy transition’. With more than 30 sessions on energy scenarios, energy finance, making a just transition, technological innovation and electrification, International Energy Week 2024 covered lots of ground.

- China is forecast to dominate global solar manufacturing capacity from 2023–2026 and is expected to continue to widen the technology and cost gap with competitors, despite local manufacturing policies in overseas markets.