New Energy World™

New Energy World™ embraces the whole energy industry as it connects and converges to address the decarbonisation challenge. It covers progress being made across the industry, from the dynamics under way to reduce emissions in oil and gas, through improvements to the efficiency of energy conversion and use, to cutting-edge initiatives in renewable and low-carbon technologies.

Europe’s market for anaerobic digestion and biogas production

8/2/2023

6 min read

Feature

The anaerobic digestion of organic wastes delivers a biogas that can be upgraded to biomethane with a variety of uses to replace fossil fuels. Paul Hudson, Senior Industry Analyst at Frost & Sullivan, takes a look at trends in the industry across Europe.

European Union (EU) countries have adopted the EU Green Deal, which aims to make Europe the first climate-neutral continent by 2050. As part of its net zero by 2050 strategy, it created policy and legislative initiatives such as the Renewable Energy Directives (RED), published in 2016 and revised in 2018 as RED II, which set a target of 32% renewables share in energy consumption and 14% renewables share in energy for the transport sector by 2030. The EU’s latest package of measures, ‘Fit for 55’, aims to reduce the EU’s greenhouse gas (GHG) emissions by 55% by 2030.

These policies favour the production and use of biogas and biomethane (which is also known as renewable natural gas, RNG) as a sustainable and green alternative to natural gas (fossil-based).

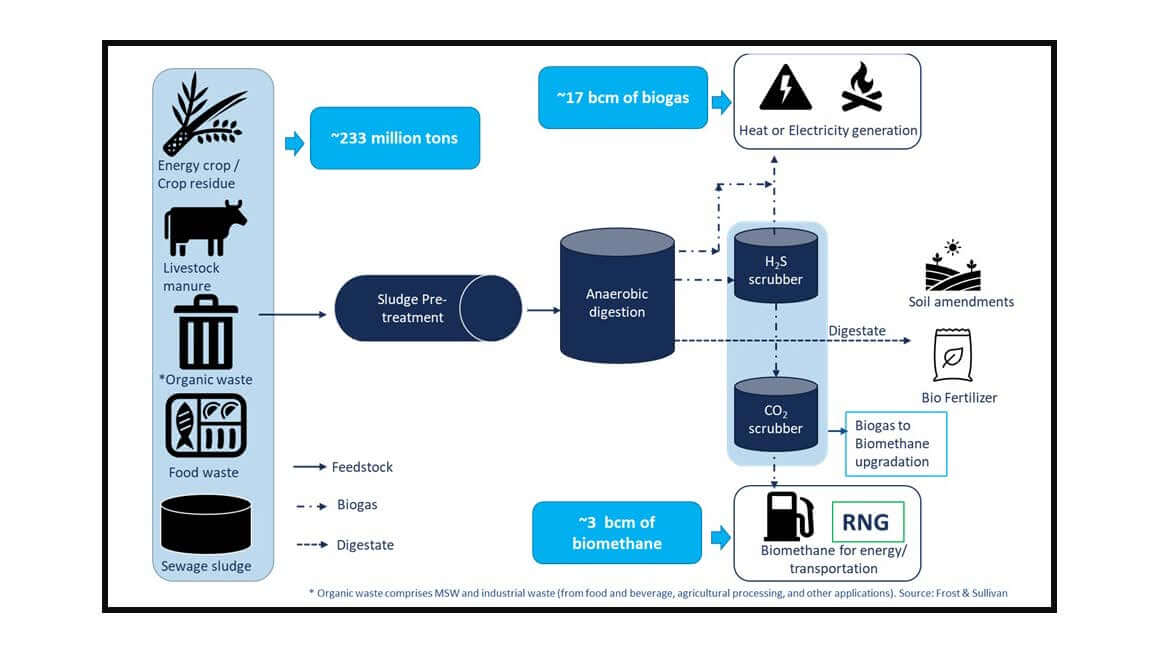

Biogas is a mixture of methane, CO2 and other impurities such as hydrogen sulphide, which is produced by the anaerobic digestion of organic matter such as livestock manure, crop residue, energy crops (eg maize), organic municipal and industrial waste, food waste and sewage sludge. Biogas can be further upgraded to get biomethane. The upgrading process involves the removal of impurities such as CO2 and hydrogen sulphide, resulting in pure methane.

Biogas can be directly used for heat and energy production, whereas biomethane, as it is identical to natural gas, can be blended with natural gas and injected into the existing gas grids. It also can also be used as fuel for transportation in the form of bio-LNG or bio-CNG.

Biogas and biomethane are renewable energy sources that can significantly reduce carbon emissions across the value chain as they help reduce and recycle waste and reduce dependence on fossil fuels. The resulting digestate from the anaerobic digestion process can be used as a fertiliser.

Biogas and biomethane will play a vital role in enabling the EU Green Deal. They are also also included in the EU taxonomy, making them eligible to receive sustainable financing.

A fresh impetus for an even faster transition to green energy came through the REPowerEU plan that was implemented to lower dependence on imported fossil fuels from Russia due to the Russia-Ukraine conflict. The plan sets an ambitious target of increasing the current production of biomethane to 35bn m3 by 2030, which was increased from a 17bn m3 target set by the Fit for 55 initiative.

Biogas can be directly used for heat and energy production, whereas biomethane, as it is identical to natural gas, can be blended with natural gas and injected into the existing gas grids, or used as fuel for transportation.

Germany leads in Europe

Since the 1950s and 1960s, the production of biogas through anaerobic digestion of biomass (organic waste or energy crops) has witnessed significant attention. Germany developed policies to favour the production of biogas for electricity production and heating, making it a leader in biogas production across the globe, with over 9,000 biogas plants (through anaerobic digestion) in operation as of 2021.

Denmark and the UK followed suit with similar policies and significantly increased their overall biogas production. As of 2021, these three countries combined had an installed base of 68% of the total anaerobic digestion/biogas production plants in Europe.

During the past five years, Germany, Denmark and the UK have modified their subsidy programmes and policies to favour biomethane production from biogas to diversify gas sources and meet their green energy transition targets. Focusing on modified policies enabled the injection of biomethane into the existing gas grid to be used for heat or energy production, and the use of biomethane (as compressed bio-CNG or liquefied bio-LNG) in transportation or other heavy-duty applications in line with their respective goals to become carbon neutral within the next decade.

Due to the drawdown of subsidies (ie withdrawal of feed-in tariffs for all plants above 100 kW), Germany witnessed a decline in new anaerobic digestion plants for biogas production since 2015. The lack of new investment has been exacerbated due to stringent regulations governing the construction of anaerobic digestion plant and continual debate concerning the use of energy crops as feedstock for biogas production – since energy crops are used as the primary source in most plants.

Leading biogas producers in Germany are now exploring new opportunities to consolidate biogas production of small and medium-sized plants and develop a centralised biogas-to-biomethane upgrading facility, as biomethane has comparatively higher value and demand as a viable replacement to natural gas for electricity, heating and transportation needs. As part of vertical expansion and value addition, industry players are also exploring opportunities to sequester CO2 for use by food and beverage industries and to produce green hydrogen.

In the last decade, France, Italy, Poland, Spain, Austria, the Netherlands and a few Eastern European countries significantly invested in biogas production with a special focus on upgrading biogas to biomethane. As of 2022, France has the highest installed base of biomethane plants (ie biogas plants with a facility to upgrade biogas to biomethane) with a total of 365 facilities. France implemented its feed-in tariffs for biogas in 2011 and adjusted for inflation in 2022, favouring growth in investment into new anaerobic digestion plants.

As of 2022, over 1,000 new anaerobic digestion plants (for biomethane from biogas) are being developed, with an estimated combined capacity of 20 TWh/y. After completing these projects, France will become the leading destination for biomethane production. As part of its multi-year energy plan, the country aims for 10% of its total natural gas demand to be from biomethane.

Italy, Poland, Spain, the Nordics and the Netherlands are set to become fast-growing markets for anaerobic digestion plants to ensure the transition to renewables and leverage existing feedstock resources. Sweden is one of the leaders in using biogas for transportation, with 64% of the biogas available in the country used by the transport sector. In 2021, 25% of Denmark’s natural gas demand was from biogas produced locally; at this pace, 75% of Denmark’s gas needs will be met by biogas by 2030.

Feedstock issues

The feedstock source used to produce biogas has played a key role in the viability and sustainability of an anaerobic digestion plant. RED II emphasises the use of sustainable feedstock (used for biofuels, including biogas, in the transportation sector) such as organic waste, agricultural waste or livestock manure, and the reduction of dependence on energy crops. Further EU directives, such as the Landfill Directive, set a target to reduce the landfilling of waste to 10% of the total waste generated, encouraging recycling, reuse and the diversion of organic waste (segregated municipal waste, food waste, organic industrial wastewater) to anaerobic digestion or composting.

Countries like Germany and the UK have primarily been dependent on the use of energy crops (specifically maize) for biogas production. Compared to other feedstocks such as livestock manure, agricultural waste, food waste, municipal solid waste and sewage sludge, energy crops have the highest methane yield and are the most favourable. However, the sustainability of using energy crops has long been questioned as it comes at the cost of other valuable crop production needed for nutrition.

Due to these concerns, Germany, Denmark and the UK have modified their premiums or subsidies to draw down dependence on energy crops. Over 60% of all new upcoming anaerobic digestion plants in the UK are set to have food waste, organic waste or livestock manure as their primary feedstock. From 2018 onward, Denmark cut down subsidies for biofuels derived from energy crops.

Similar initiatives in the form of additional premiums for livestock manure, agricultural waste, sewage sludge, and organic waste as primary feedstock have been implemented in France, Italy, Spain, Poland and the Nordics.

Anaerobic digestion and biogas production value chain in Europe

Source: Frost & Sullivan

Growth and expansion

Europe is currently at the forefront in enabling the growth and expansion of the anaerobic digestion and biogas production market. In the past three years, the market has witnessed a convergence among technology solution providers, project developers, producers and off-takers across the value chain.

In 2021, multinational energy company TotalEnergies partnered with Veolia, a water and wastewater treatment solution provider, to invest in and develop biomethane production facilities in wastewater treatment plants in 15 different countries, to produce 1.5 TWh/y by 2025. Meanwhile, multinational oil and gas company Shell acquired Nature Energy, the largest producer of biomethane in Europe. Shell will use Nature Energy to expand its existing biomethane production capability to cater to the demand for cleaner fuels. This signifies the value of anaerobic digestion technology aligned with EU green taxonomy.

Frost & Sullivan estimates that the European anaerobic digestion and biogas production market is set to grow to $54bn by 2030, from $27bn in 2022, with a compound annual growth rate of 9.1%. The company estimates that 70% of the total revenue is from biogas/biomethane production, 5% is from revenue generated from feedstocks (ie received as tipping fees), and the rest is the revenue generated from the sale of anaerobic digestion and biogas production technology solutions.